Gold outlook – gold to flatline out to June 2019 in the absence of shocksby Nitesh Shah, Director, Research

Although the environment of elevated geopolitical risk is normally associated with higher gold prices, recently very little of that anxiety has been expressed in gold. Gold is being weighed lower by a rising interest rate environment in the US. An appreciation of the US Dollar (up 1.6% over the past month) is also weighing on the yellow metal’s performance. Given the soft patch of economic data from Europe and Japan, interest rates are likely to diverge between the US and other countries, leading to further dollar appreciation and negative gold price pressure.

Looking ahead, we believe gold’s price is likely to flatline until mid-2019, unless unexpected shock events result in a sudden drive towards safe-haven assets.

Recently, we updated our forecasts for gold, using the framework first described in the report “Policy mistakes provide upside potential for gold”, published in January 2016. For a detailed description of the new forecasts, please click here. Below we present a summary of our new base, bull and bear case gold price forecasts.

Base case

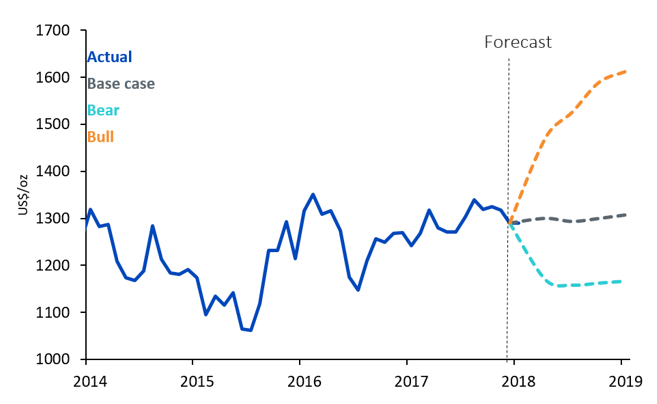

In our base-case scenario, gold is likely to flatline out to the end of June 2019, ending the period at a price of $1,307/oz, close to gold’s price of $1,294/oz gold, at the time of writing.

We assume that the US Federal Reserve (Fed) is on track to raise to interest rates at least four times by the end of June 2019. In our base-case scenario for gold, inflation is likely to remain above-target, providing some support for the precious metal, yet rising interest rates and US dollar appreciation will weigh on performance. Our base case also assumes that we see no unexpected shock events between now and mid-2019.

Figure 1: Gold price forecast

Source: Bloomberg, WisdomTree, data available as of close 30 May 2018. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties. You cannot invest directly in an Index.

Bull case

In our bull-case scenario, gold could rise to $1,613/oz by the middle of 2019.

Our bull-case scenario assumes that the Fed is more relaxed about inflationary pressures, extrapolating this period of tight market conditions without wage and inflationary repercussions. Treasury yields decline in this scenario. We also revert to the consensus view of the US dollar depreciating.

- Gold markets incorporate a number of geopolitical risk including:

- Continued tension between US/Japan/South Korea and North Korea

- An escalation of the proxy war between Saudi Arabia and Iran, with Iran withdrawing from the Joint Comprehensive Plan of Action (JCPOC) and resuming its nuclear programme

- A disorderly unwinding of credit in China

- Italian policy paralysis as a result of the country’s inability to form a functional government

- Market volatility, with the VIX (equity) or MOVE (bonds) indices spiking as yield trades unwind

Bear case

In our bear-case scenario, gold falls to $1,166/oz by June 2019.

Our bear case assumes that the Fed becomes more aggressive in tackling inflationary pressures. In this scenario, the Fed tries to anchor inflation expectations amid rising headline figures that it fears could be mistaken as persistent. 10-year nominal Treasury yields rise and the US Dollar appreciates more aggressively.

Conclusion

Our model suggests that gold’s price is influenced by a number of key factors, including the value of the US dollar, inflation rates, changes in nominal yields, and investor sentiment towards the precious metal. Looking ahead, in our base-case scenario, we expect gold’s price to flatline out to June 2019, assuming an absence of sudden unexpected events that shock global financial markets. However, should events turn out differently and some of the geopolitical concerns crystallise into an adverse shock, gold could trade substantially higher. Thus, with gold currently trading at US$1294/oz at the time of writing, investors concerned about adverse geopolitical shocks may have found a good entry point.

To read the detailed report of our new forecasts, please access the document below.

Gold Outlook June 2018

Disclaimer

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Please click here for our full disclaimer.

View our Conflicts of Interest Policy and Inventory here.